Banks' earnings are currently mainly padded by providing mortgages to private homebuyers. While margins on other products are actually falling, margins on mortgages are rising. Property buyers are thus footing the bill for low interest rates for the banks. As banks compensate for this difference, there is no negative interest rate as yet. This is unlike in Denmark, where mortgage rates are now even negative.

Recently, interest rates broke one record low after another. Especially now that more stimulus measures have been announced by the ECB. Negative interest rates have become the norm in 2019. Banks face a new challenge as a result. Most of their earnings are realised by attracting cheap capital from savers and lending it out at higher interest rates. But the question is what happens when market interest rates fall below zero and negative savings rates are not an option for now for fear of dissatisfied customers. How will profits then be maintained?

Property buyers play an important role in this. Several banks stated in their half-year results that they were satisfied that they made more money on mortgages. This is caused by banks hardly passing on the lower interest rates to their customers. ABN Amro is leading the way in this by raising interest rates and gaining market share in the mortgage market. This is in contrast to banks in Denmark. Indeed, Scandinavian bank Nordea is going to offer residents of Denmark mortgages with a 20-year fixed rate at 0% interest. At 10 years, the interest rate is even negative at -0.5%.

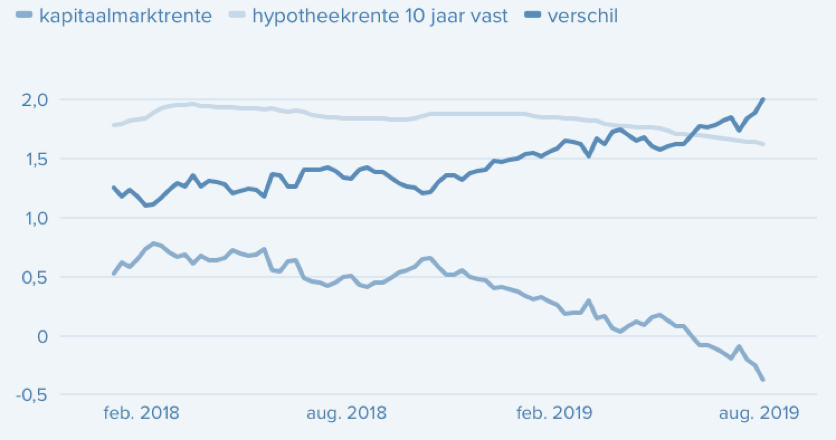

Netherlands real estate buyers are taking less advantage of low market interest rates. Banks are buying almost negative money. The interest rate paid by banks has proportionally fallen much harder than mortgage rates. Traditionally, mortgages are an important source of income, but the widening gap between market and mortgage interest rates makes mortgages even more important. Incidentally, it also applies to other lenders, including pension funds and insurers, among others, which pass on lower market interest rates only to a limited extent.

The Danish situation is different, as in Denmark most mortgages are traditionally financed with special, typically Danish mortgage bonds. According to a fixed formula, the interest the homebuyer has to pay is linked to the interest rate on those bonds, so mortgage rates follow market rates faster than in the Netherlands.

Source: https://fd.nl/ondernemen/1311513/huizenbezitter-redt-banken-in-lagerentetijdperk, https://fd.nl/ondernemen/1311237/deense-hypotheekrente-twintig-jaar-lang-op-nul